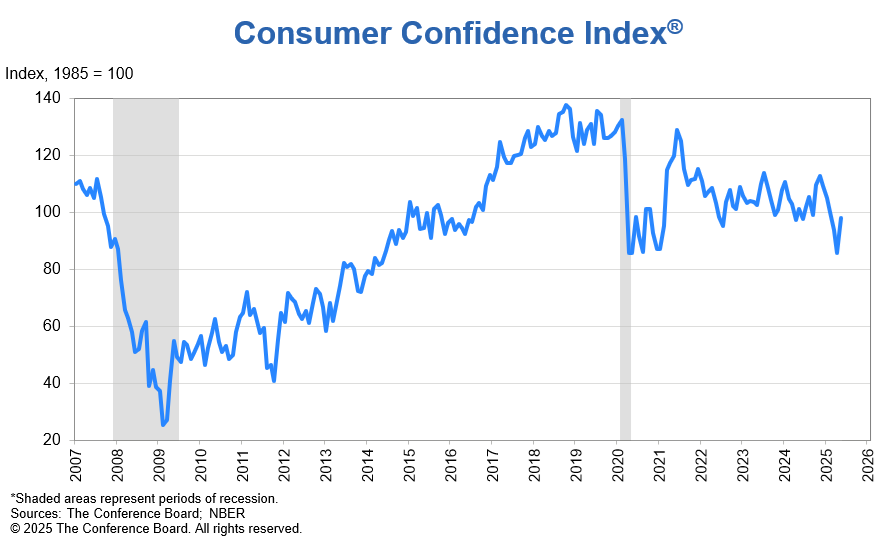

NEW YORK — After five straight months of decline, U.S. consumer confidence showed signs of revival in May, offering a cautiously optimistic signal for the retail industry ahead of the summer.

According to the latest Consumer Confidence Survey from The Conference Board, the Consumer Confidence Index jumped 12.3 points to 98.0, reversing a sharp drop in April. The rebound was primarily fueled by improving consumer expectations following the May 12 announcement of a partial pause on tariffs targeting Chinese imports, an issue that has weighed heavily on household sentiment.

“Consumer confidence improved in May after five consecutive months of decline,” said Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board. “The rebound was already visible before the May 12 US-China trade deal but gained momentum afterwards. The monthly improvement was largely driven by consumer expectations as all three components of the Expectations Index—business conditions, employment prospects, and future income—rose from their April lows. Consumers were less pessimistic about business conditions and job availability over the next six months and regained optimism about future income prospects. Consumers’ assessments of the present situation also improved. However, while consumers were more positive about current business conditions than last month, their appraisal of current job availability weakened for the fifth consecutive month.”

Guichard added: “With the stock market continuing to recover in May, consumers’ outlook on stock prices improved, with 44% expecting stock prices to increase over the next 12 months (up from 37.6% in April) and 37.7% expecting stock prices to decline (down from 47.2% in April). This was one of the survey questions with the strongest improvement after the May 12 trade deal.”

Retailers may find encouragement in improving consumer attitudes toward spending. Plans to buy big-ticket items such as appliances and electronics increased, along with intentions to travel and dine out. Spending intentions rose across nearly all service categories, with notable jumps in entertainment and leisure activities like movies, live shows, and sports events.

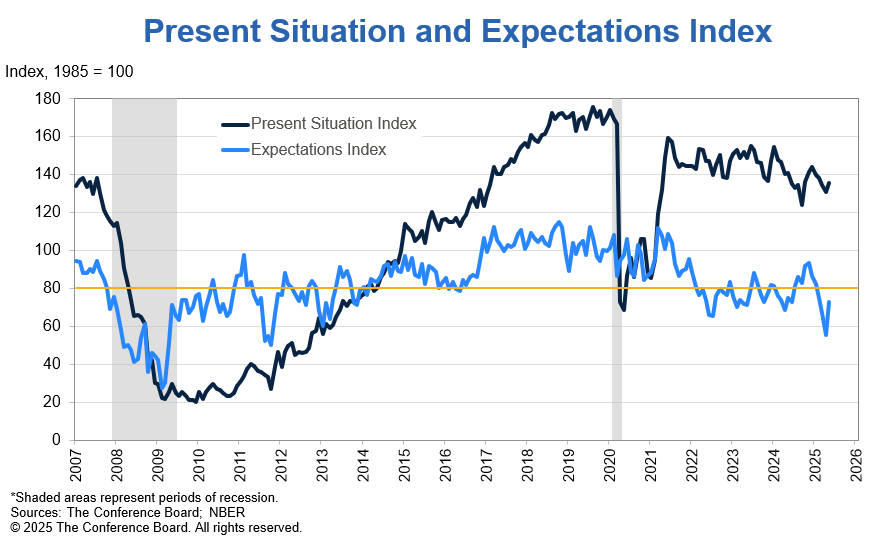

The Present Situation Index, which assesses current business and labor market conditions, also climbed 4.8 points to 135.9. However, job market perceptions were mixed: while slightly more consumers said jobs were "plentiful," the share saying jobs were "hard to get" also rose.

Consumers’ assessments of current business conditions improved in May.

- 21.9% of consumers said business conditions were “good,” up from 19.2% in April.

- 14.0% said business conditions were “bad,” down from 16.3%.

Consumers’ views of the labor market weakened in May.

- 31.8% of consumers said jobs were “plentiful,” up slightly from 31.2% in April.

- 18.6% of consumers said jobs were “hard to get,” up from 17.5%.

Expectations Six Months Hence

Consumers were less pessimistic about future business conditions in May.

- 19.7% of consumers expected business conditions to improve, up from 15.9% in April.

- 26.7% expected business conditions to worsen, down from 34.9%.

Consumers’ outlook for the labor market outlook was also less negative in May.

- 19.2% of consumers expected more jobs to be available, up from 13.9% in April.

- 26.6% anticipated fewer jobs, down from 32.4%.

Consumers’ outlook for their income prospects turned positive in May.

- 18.0% of consumers expected their incomes to increase, up from 15.9% in April.

- 13.8% expected their income to decrease, up from 17.7%.

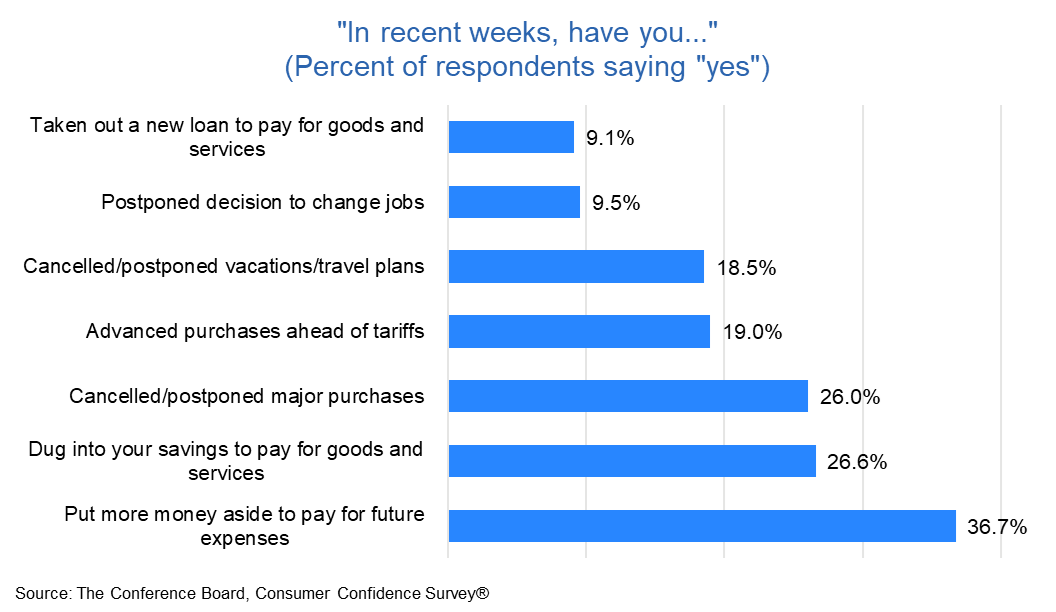

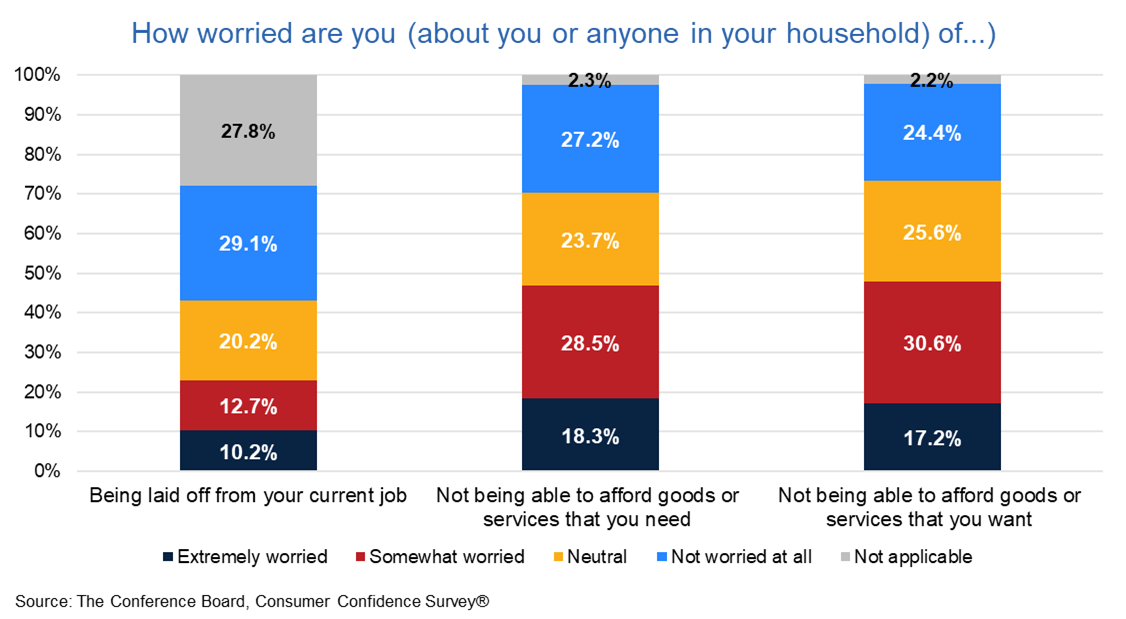

Consumers’ concerns about affordability are growing, even as fears of job loss remain subdued. Nearly half of the survey respondents expressed anxiety about being unable to afford what they need or want, compared to less than a quarter who feared layoffs. This signals a shift in focus from job security to purchasing power, an essential consideration for pricing and promotions in the months ahead.

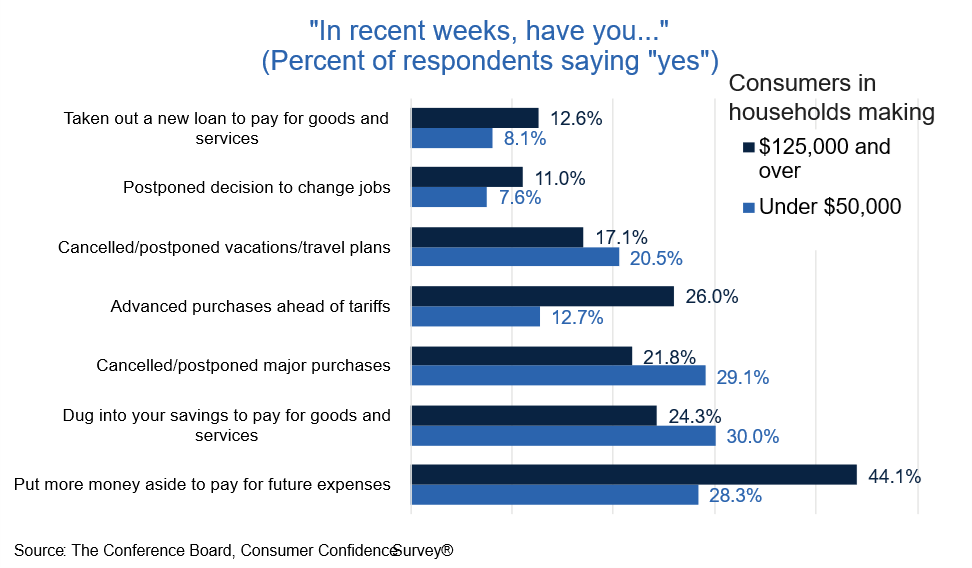

Importantly, high-income households appear to be driving a significant part of the rebound. Consumers earning over $125K were more likely to report saving for future spending and showed a greater propensity to shift purchases ahead of potential tariffs. Meanwhile, lower-income consumers continued to report tapping into savings and postponing major purchases.

While inflation and high prices remain at the top of the mind, the report hints at early signs of relief: inflation expectations eased slightly to 6.5% from 7% in April, and some consumers noted lower gas prices.

Key Takeaways for Retailers:

- Confidence Rebounds: Index rises to 98.0 as consumers regain optimism.

- Spending Plans Improve: Increased intent to buy cars, appliances, and take vacations.

- Affordability Tops Concerns: More worry about price pressure than job security.

- High-Income Households Lead Rebound: More likely to save or advance purchases.

With rising consumer sentiment and renewed interest in discretionary spending, retailers can capture renewed demand, primarily in categories like dining, streaming, travel, and entertainment, as the summer shopping season unfolds.

{kind=link}