CHARLOTTE, N.C. — A growing number of Americans are turning to “buy now, pay later” (BNPL) loans to finance their grocery purchases, with more borrowers struggling to pay those loans back on time, according to a new Lending Tree survey released Friday.

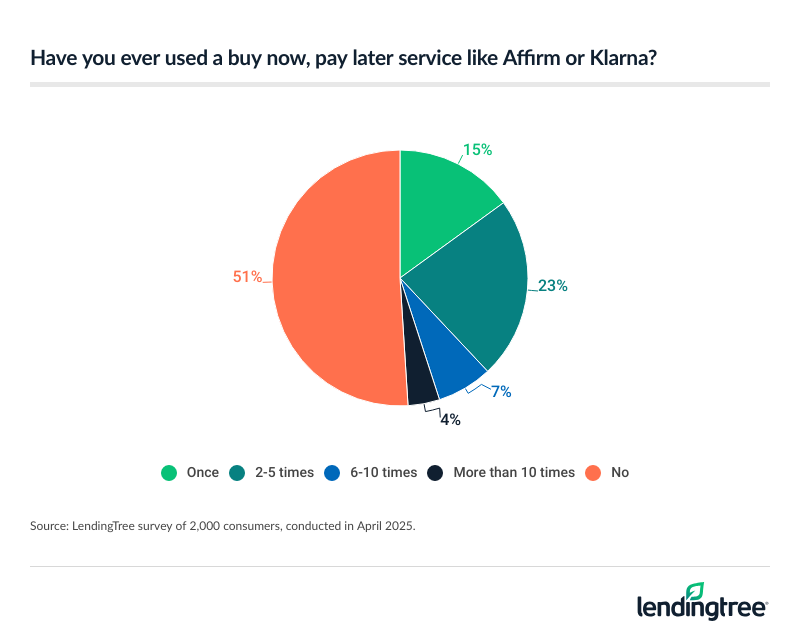

The survey, conducted earlier this month among 2,000 U.S. adults aged 18 to 79, found that 25% of BNPL users said they had used the loans to buy groceries, up from 14% in 2024 and 21% in 2023. At the same time, 41% of respondents reported making an overdue payment on a BNPL loan within the past year, up from 34% the previous year.

The findings offer another warning sign that consumers are feeling the squeeze from persistent inflation, high interest rates, and growing economic uncertainty, including concerns over new tariffs.

“It’s pretty clear that as people struggle with inflation and other kinds of economic uncertainty, people are looking to things like BNPL loans to help them extend their budget,” Matt Schulz, Lending Tree's chief consumer finance analyst, told Fortune.

“When buy now, pay later started, it was typically about designer handbags and appliances and things like that,” Schulz said. “But now, people are looking at it for things like groceries and food delivery.”

While BNPL loans — typically structured to allow consumers to split payments into several installments, often interest-free — can offer temporary relief, they carry risks. Missing payments can trigger high fees, and stacking multiple BNPL loans can quickly lead to debt spirals. Lending Tree’s survey found that 60% of BNPL users had multiple loans at once, and nearly a quarter had three or more active simultaneously.

The rising use of BNPL services for everyday essentials, rather than luxury goods, may signal deeper shifts in consumer behavior. Originally popular for financing higher-end purchases like designer handbags and electronics, BNPL is now being used for basic necessities like groceries and food deliveries. Companies such as DoorDash recently announced partnerships with BNPL providers like Klarna, allowing customers to finance their takeout meals — a move that sparked jokes about Americans now “financing cheeseburgers and burritos.”

At the same time, a recent Billboard survey found that 60% of Coachella festivalgoers funded their general admission tickets using BNPL services, fueling concerns that many consumers are using debt to sustain their lifestyles.

Amid these signs of financial strain, broader consumer sentiment has also weakened. The consumer confidence index recently fell to 52.2, down from 57 a month earlier, and an Associated Press-NORC poll found that half of Americans are now “extremely” or “very” concerned about a looming recession.

While Schulz stopped short of declaring the BNPL data a recession indicator, he warned that economic conditions will likely deteriorate before they improve.

As BNPL becomes more embedded in everyday financial habits — especially among younger and higher-income users — experts warn that the apparent convenience masks real risks, including debt accumulation and the lack of credit-building opportunities.

Despite these risks, Schulz expects the popularity of BNPL to continue growing. “I don’t think there’s any reason to believe that this is going to do anything but increase,” he said.