CHICAGO – U.S. beauty industry performance was nearly on par across both the prestige and mass retail channels in the first quarter, according to data from Circana.

Prestige retail dollar sales of $8.1 billion were up 6% from the first quarter of 2025. Sales at mass retailers increased 7% to $18.1 billion, Circana said.

Unit sales through both channels increased in the low single digits.

Growth in both channels was largely value‑driven, the firm reported, with dollar growth outpacing units, reflecting both premiumization and selective consumer spending.

“Mass and prestige beauty are growing at nearly the same rate for the first time in five years,” said Larissa Jensen, global beauty industry advisor at Circana. “Fragrance, facial skin care, hair treatments, and personal care products like body lotion and wash continue to benefit from consumers prioritizing self-care, elevated routines, and wellness driven products. We expect these areas to remain strong this year, as shoppers continue to shop across channels, seeking affordable yet high performing beauty products that feel good and work well.”

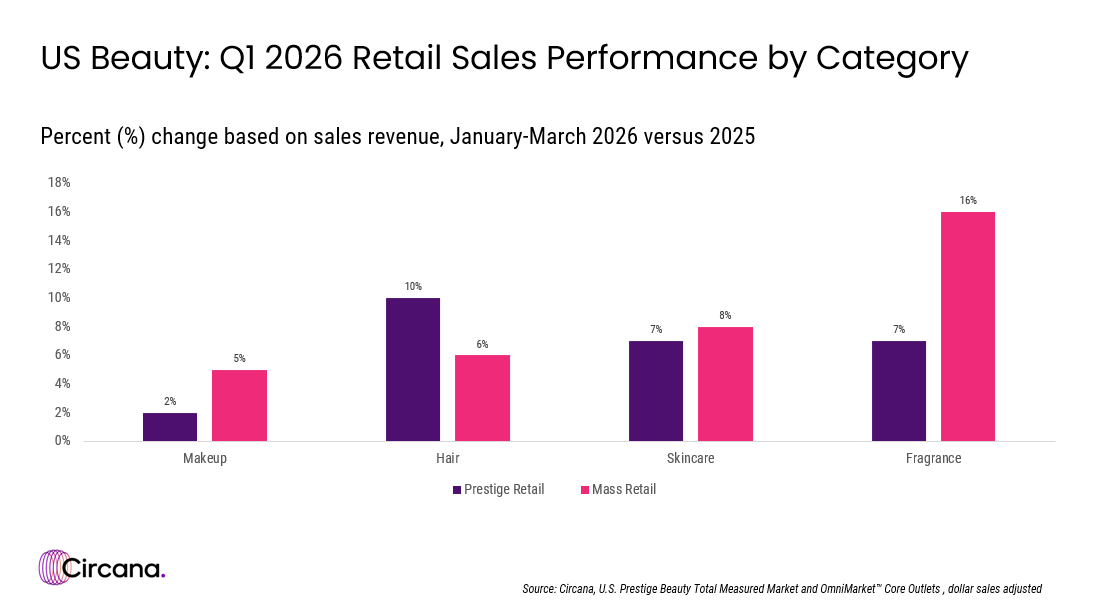

Makeup was the softest-performing category in the year’s first quarter. Both prestige and mass retailers notched modest dollar growth offset by declining unit demand, which was particulary notable in the mass channel, Circana said, while noting pockets of strength in lip and face.

Lip treatments and lip liner stood out as top performers in both channels, delivering growth in both dollars and units, while blush and bronzer also posted solid gains.

The hair category showed a clear channel divide – in prestige, it was the fastest-growing category by dollars and a top unit driver (second only to skin care), fueled by continued strength in treatments. In mass, value-seeking behavior drove double-digit growth in shampoo and conditioner combo packs.

Skin care remained a steady growth engine, with prestige gains led by facial care; face creams, serums, and eye treatments collectively drove the majority of category growth.

In addition, clinical brands captured over one-third of dollar sales, reinforcing the importance of science-backed positioning. Skin care also showed broad-based strength at mass retail, with nearly all face and body segments growing in both dollars and units.

Fragrance was among the strongest performers overall, with gains across both channels: in mass, growth was driven by double-digit increases in women’s fragrances, while in prestige, higher-value formats, luxury offerings, and continued momentum in minis (also growing double digits) underscored both trade-up and trial-driven behaviors.

Online and social shopping continue to capture share of beauty retail, reinforcing a structural shift in how consumers discover, trial, and replenish products.

In the prestige market, online sales outperformed brick‑and‑mortar across all major categories in the first quarter. Skin care delivered the most notable inflection point, with e‑commerce now accounting for nearly half of prestige dollars and the majority of units sold.

Social commerce is further accelerating this shift, with beauty emerging as the dominant category on TikTok Shop in 2026. Fueled by live shopping events and promotional moments, beauty and personal care led all categories in the first quarter, capturing 20% of TikTok Shop dollar spending.

Launched in late 2023, TikTok Shop already represents 10% of total beauty e‑commerce sales, underscoring its rapid ascent as a meaningful retail channel, Circana said.

“Digital and social platforms are no longer just a testing ground for emerging brands; they are full‑scale commerce engines,” said Jensen. “For both established players and smaller brands, success increasingly hinges on how effectively digital and social plans are embedded into marketing and product strategies. Rather than optional or additive, these platforms must be foundational to how brands build relevance, drive demand, and scale growth.”

Submit Your Press Release

Have news to share? Send us your press releases and announcements.

Send Press Release

{kind=link}